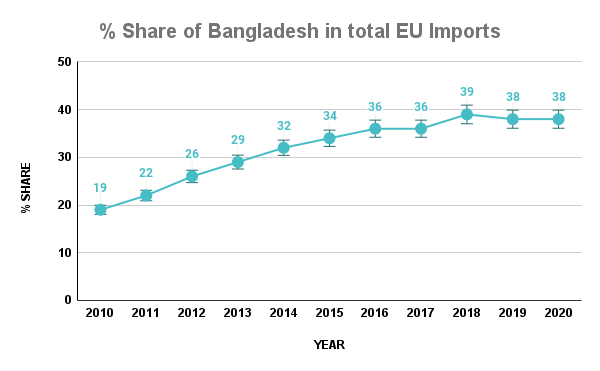

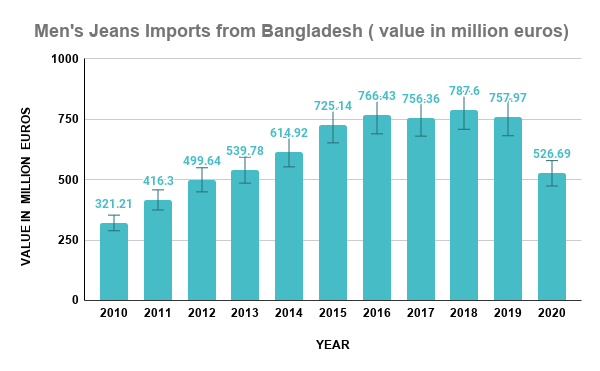

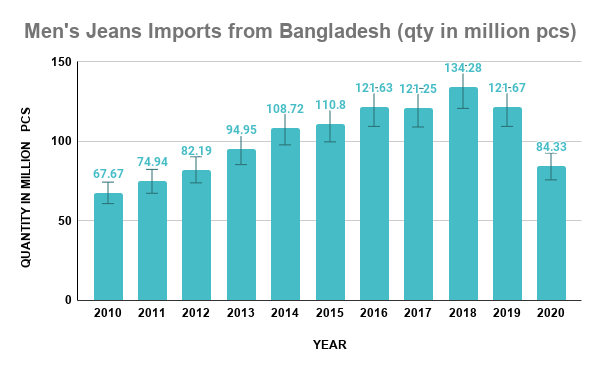

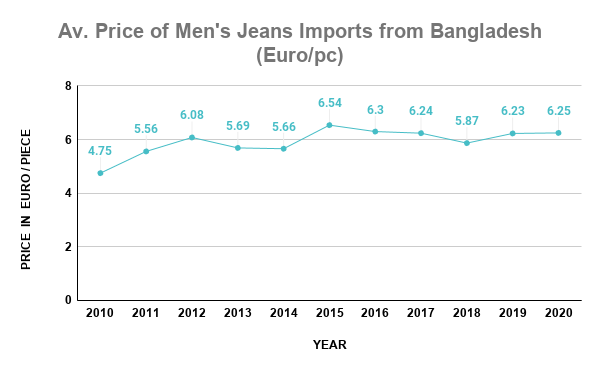

The denim market in the UK serves as a significant chapter in the global fashion narrative, distinguished by intricate supply chains and calculated retail strategies. This report examines the intricate web of transactions between the UK’s retail giants and their Bangladeshi suppliers, focusing on the period between September 2022 and September 2023. We examine four critical aspects: the comparative supplier overview, a detailed analysis of the suppliers to the top brands, fiscal year import figures, and a broader market analysis. Our assessment aims to decode the purchasing patterns, quantify the volume and values, and provide clarity on the market positions of the suppliers involved.

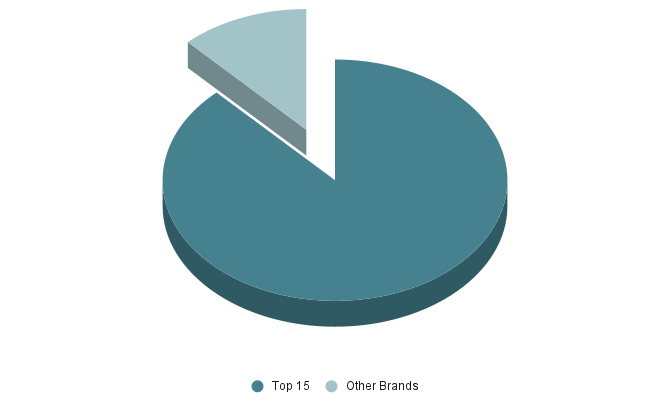

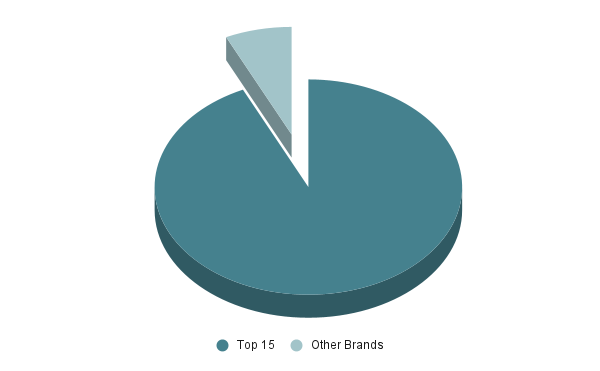

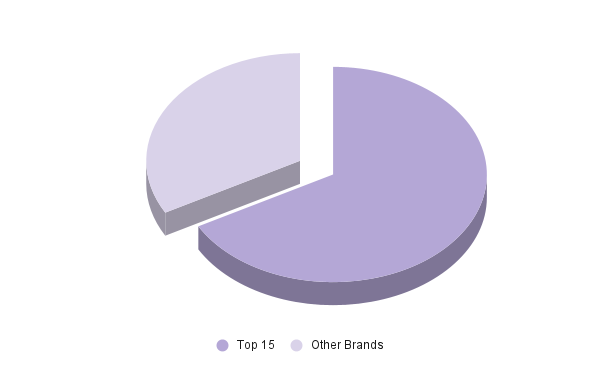

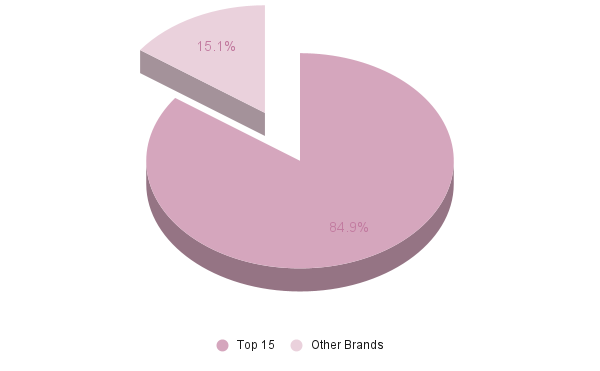

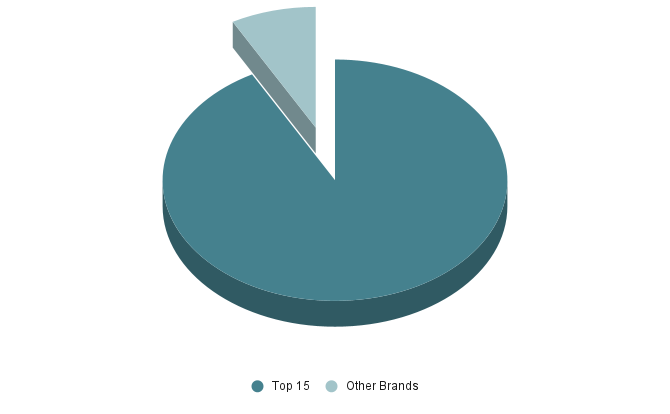

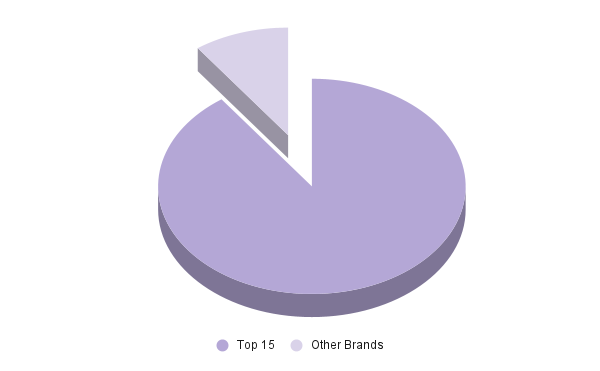

One of the key highlights is that major UK brands accounted for an impressive 90% of the overall denim purchased from Bangladesh.

[private_special] Note: This report only reflects the shipments that were made to United Kingdom. If any shipments were made by these brands to other destinations, they would not be covered here.

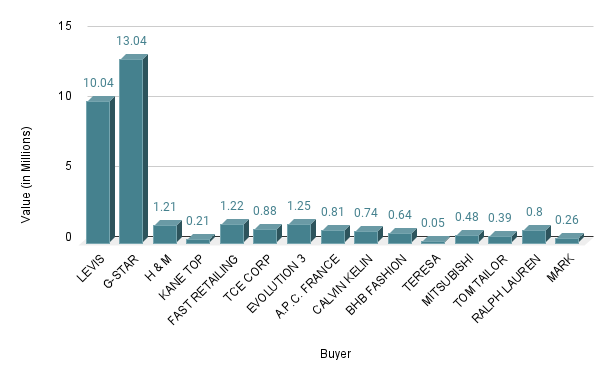

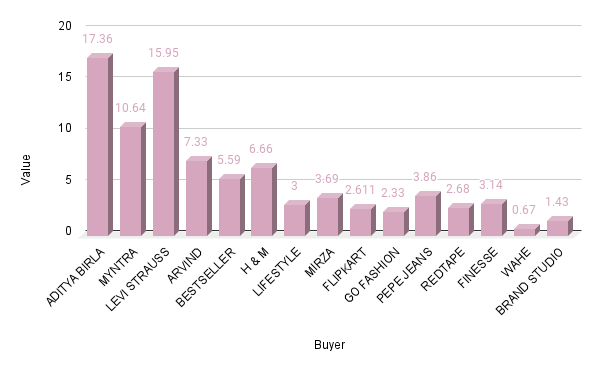

Top Brands Dominating the UK Denim Purchases From Bangladesh

The denim market in the UK has been largely influenced by several key players in the retail sector. This analysis covers the period from September 2022 to September 2023, focusing on the brands that have imported denim garments from Bangladesh to meet the demand within the UK market. It is important to note that this report only considers the denim purchases that are designated for the UK market, excluding any quantities intended for other international markets.

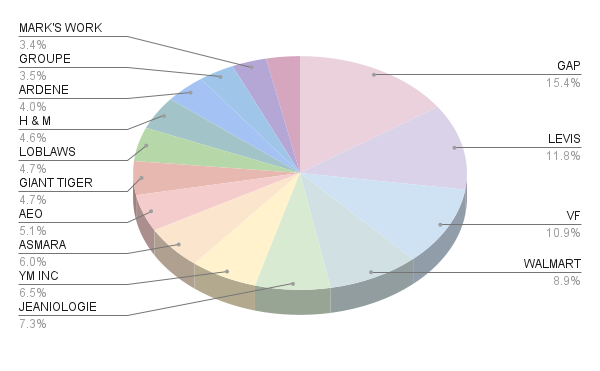

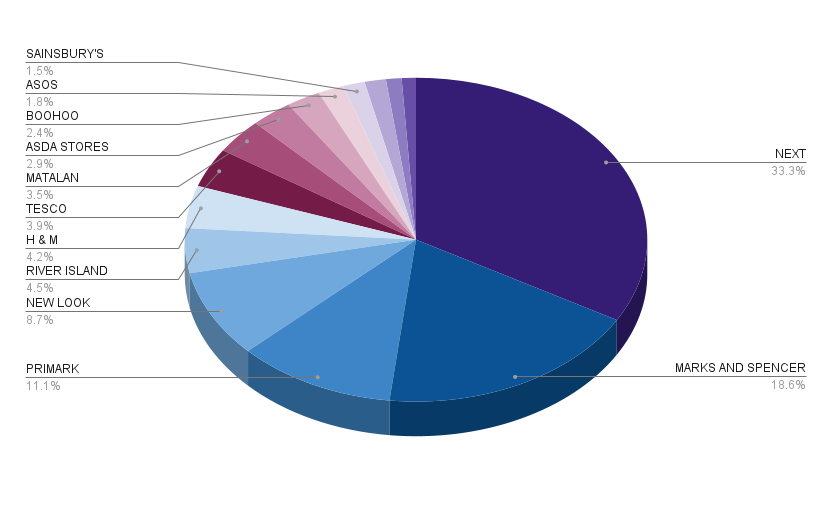

Market Share Overview – Sept’22 – Sept’23

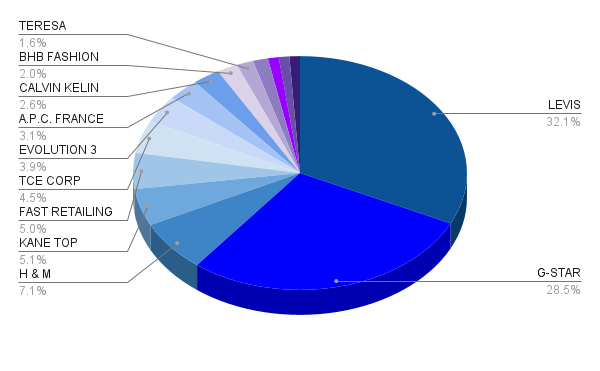

- Next: Dominates the UK market with a substantial 33.3% market share, reflecting its prominent position in sourcing denim from Bangladesh.

- Marks and Spencer: Holds a significant stake with an 18.6% share, indicating its strong reliance on Bangladeshi denim.

- Primark: Not far behind, with an 11.1% share of the imports, showcasing its notable presence in the UK denim landscape.

- Smaller yet influential shares are held by New Look at 8.7%, River Island at 4.5%, and H&M at 3.9%, each contributing to the diversity of denim offerings in the UK market.

- Other retailers like Tesco, Matalan, ASDA Stores, Boohoo, ASOS, and Sainsbury’s collectively contribute 15.7%, reflecting the competitive nature of the market with various players vying for consumer attention.

Market Insights

The dominance of NEXT in the UK’s denim imports from Bangladesh indicates a strategic alignment with Bangladeshi suppliers, likely due to favorable pricing, quality, or both. Marks and Spencer’s significant share also suggests a targeted approach to stocking their shelves with denim products that resonate with their customer base.

Primark’s strong market share further emphasizes the demand for affordable denim in the UK, aligning with the brand’s positioning as a value retailer. The presence of multiple retailers like New Look, River Island, and H&M indicates that the UK denim market is diverse, with consumers having a broad array of choices from various price points and styles.

Further sections of this report will delve into the implications of these figures and offer insights into the dynamics of the denim industry.

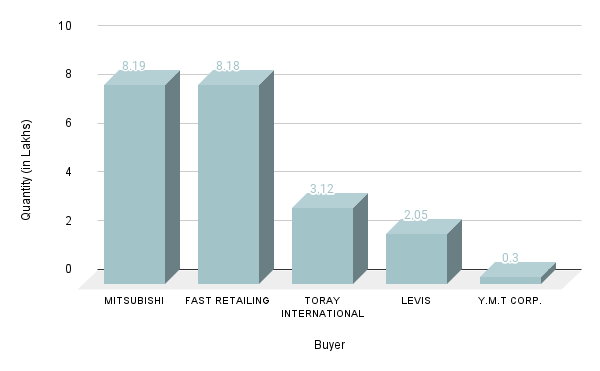

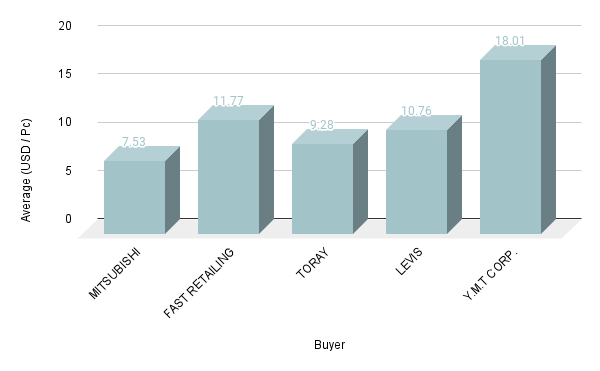

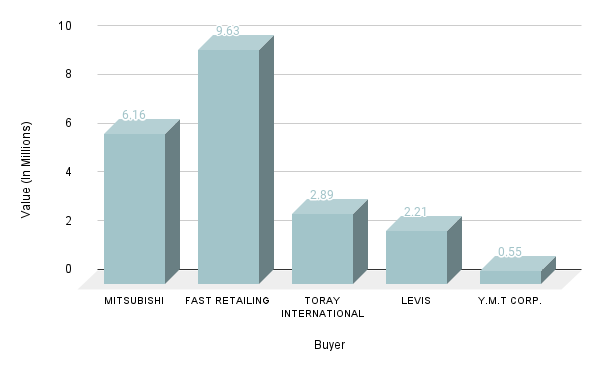

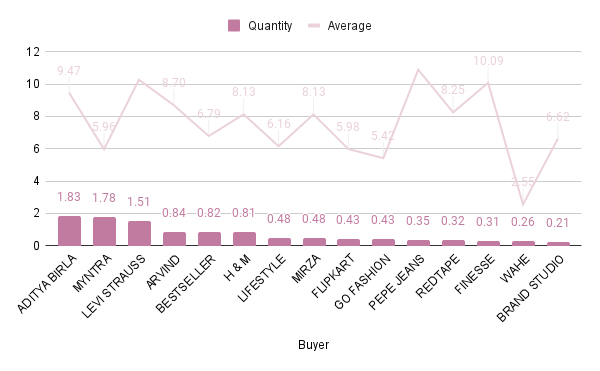

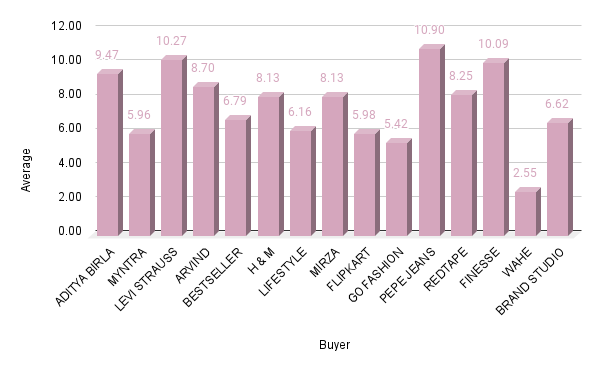

Purchasing Analysis of Top UK Companies Buying Denims

This segment of report analyzes the denim purchasing habits of the UK’s top retail companies from Bangladesh, over the period of September 2022 to September 2023. We examine the quantities purchased, average prices paid, and the total value of denim procured by each company.

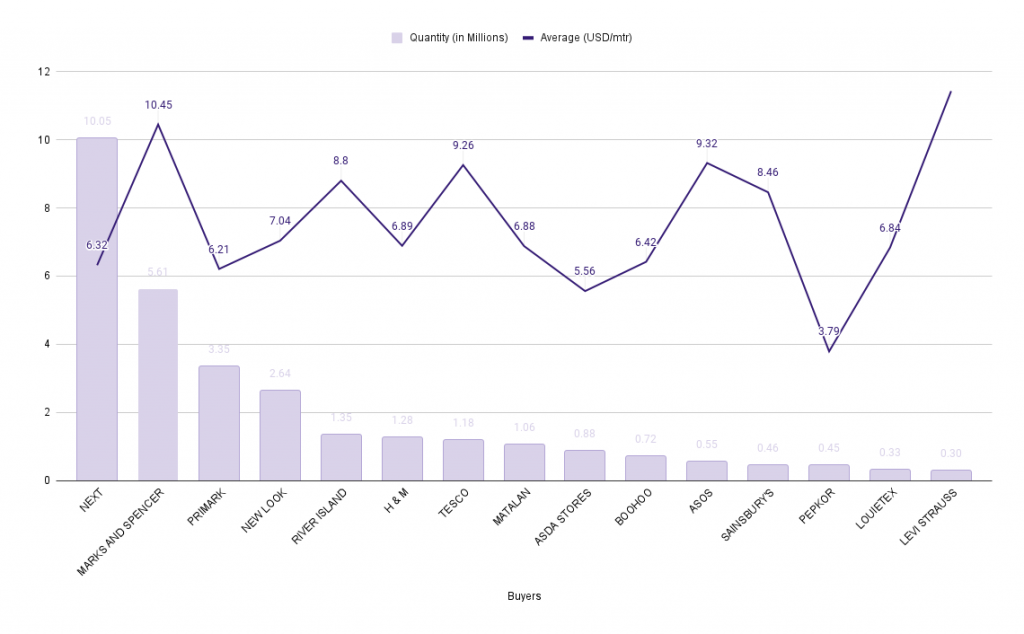

High-Volume Buyers

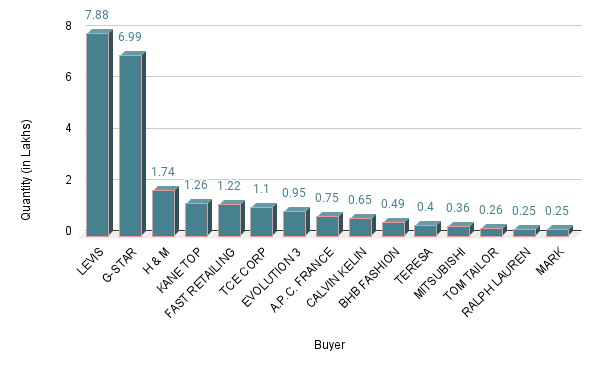

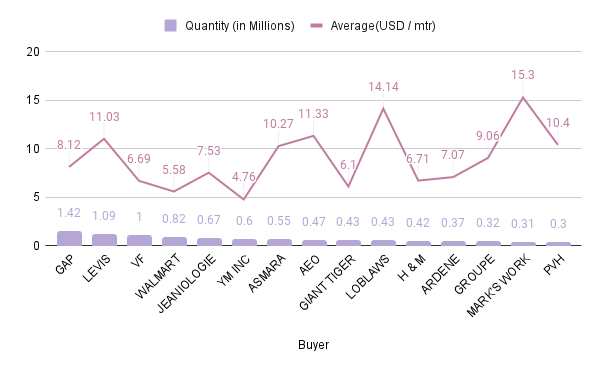

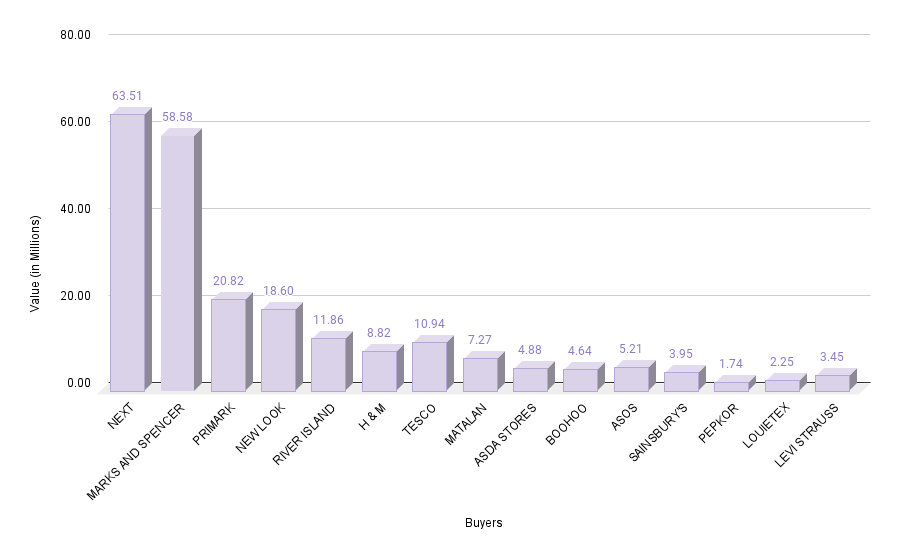

- NEXT: The leading buyer with 10.05 million units at an average price of USD 6.32 per piece, culminating in a total value of USD 63.51 million.

- Marks and Spencer: Procured 5.61 million units at a higher average price of USD 10.45 per piece, indicating a premium sourcing preference, with a total expenditure of USD 58.58 million.

Value-Focused Retailers

- Primark: Acquired 3.35 million units at a cost-effective average price of USD 6.21 per piece, amounting to a total value of USD 20.82 million.

- New Look: Purchased 2.64 million units at USD 7.04 per piece, reflecting a moderate price strategy, with a total value of USD 18.60 million

Mid-Level Purchasers

- River Island: Bought 1.35 million units at USD 8.8 per piece, with a total spending of USD 11.86 million.

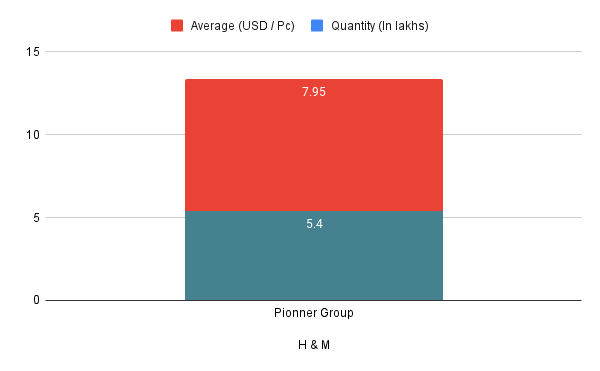

- H&M: Imported 1.28 million units at USD 6.89 per piece, totaling USD 8.82 million.

Additional Buyers

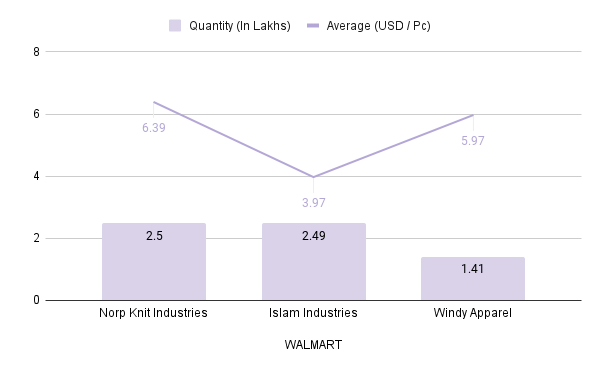

- Tesco, Matalan, and ASDA Stores: These retailers showed a balanced approach with average prices ranging from USD 5.56 to USD 9.26 per piece and total values between USD 4.88 million and USD 10.94 million.

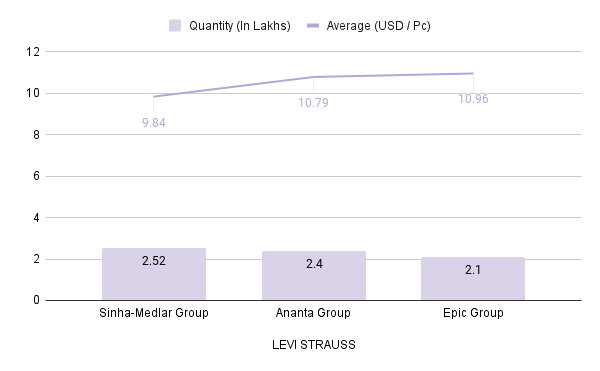

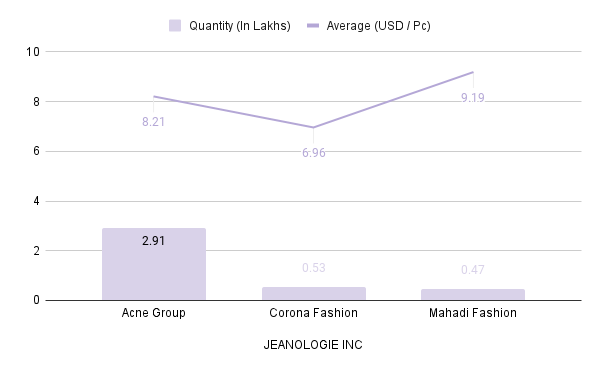

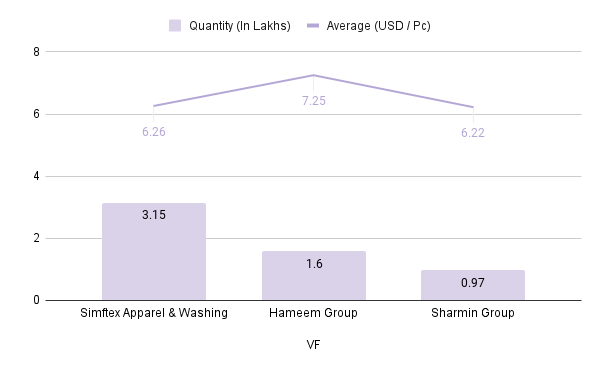

- Smaller-scale buyers such as Boohoo, ASOS, Sainsbury’s, Pepe Jeans, Louitex, and Levi Strauss varied in both quantities and average prices, indicating diverse purchasing strategies aligned with their brand positioning.

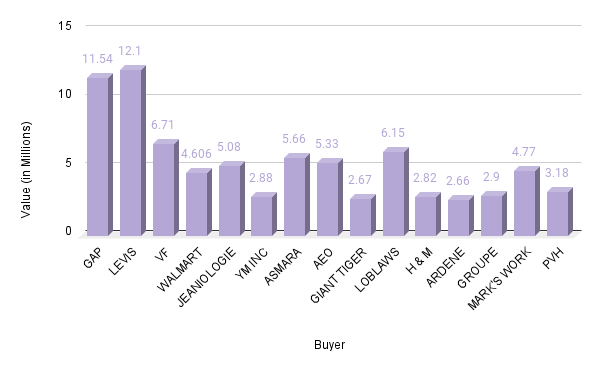

The purchasing patterns from Bangladesh indicate a dynamic UK denim market where NEXT and Marks and Spencer are leading the way in terms of volume and value, respectively. Primark’s strategy showcases a focus on affordability, while River Island and H&M occupy the mid-range market segment. The varying average prices reflect each retailer’s unique market approach, targeting different consumer demographics. This report underscores the significance of strategic buying decisions in maintaining competitiveness within the UK’s retail apparel sector.

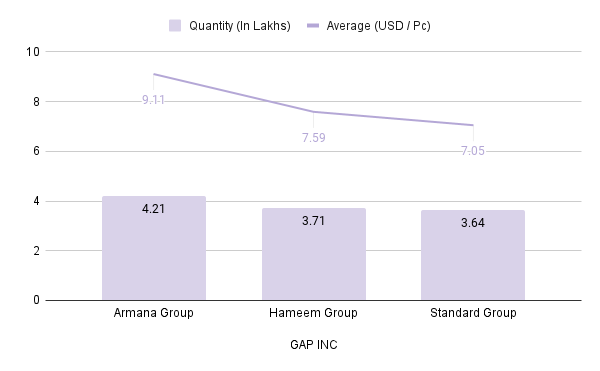

Analysis of Garment Suppliers for UK’s Top Retail Brands

This overview captures the strategic relationships between UK retail brands and their garment suppliers, highlighting how each brand aligns its sourcing strategies with its market positioning and customer base.

Supplier Insights

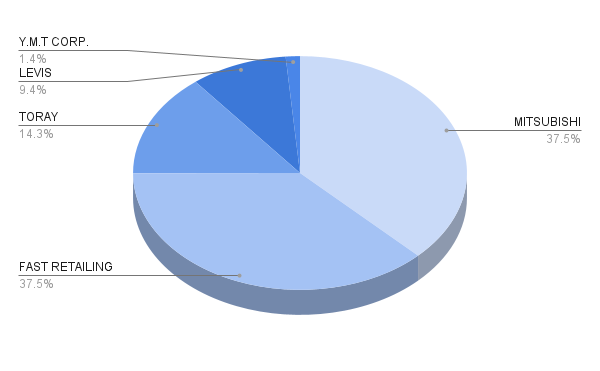

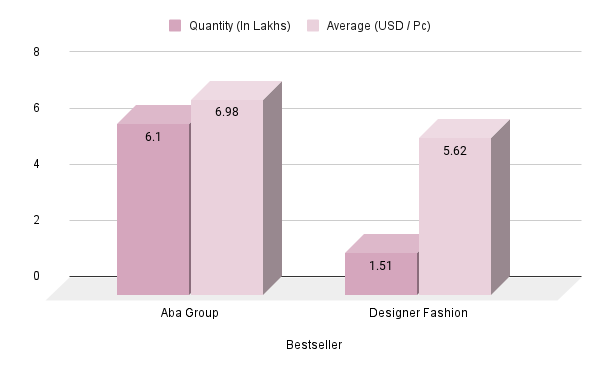

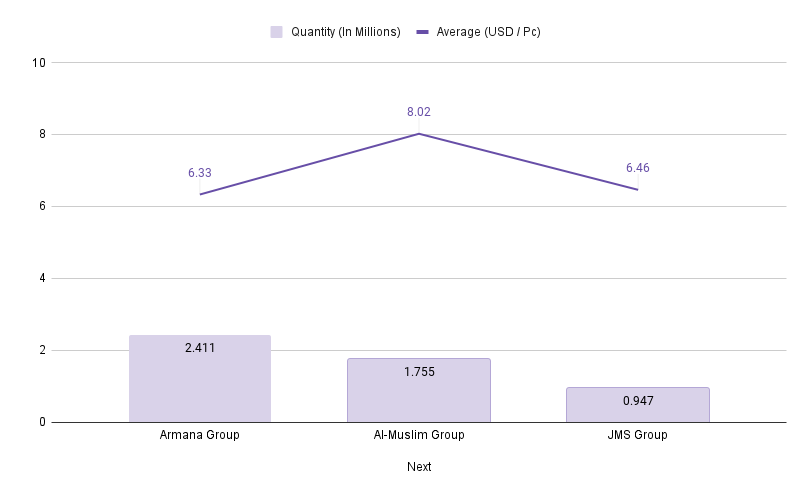

Armana Group

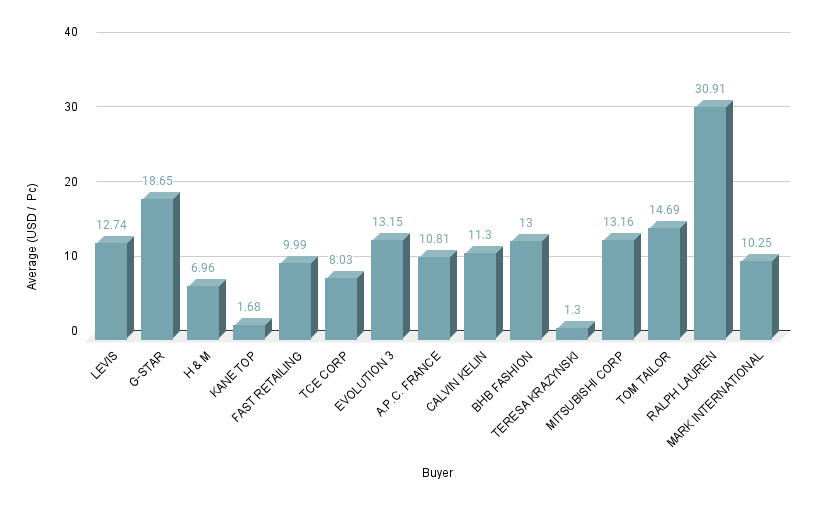

- Next: Largest contributor with 2.411 million units at the most economical average price of USD 6.33 per unit.

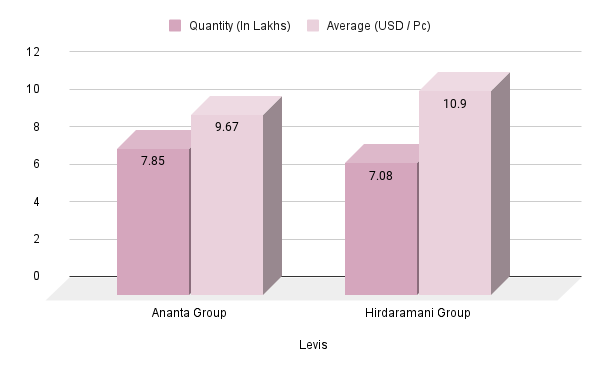

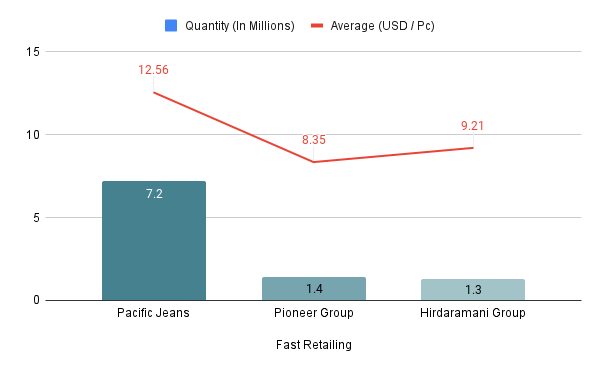

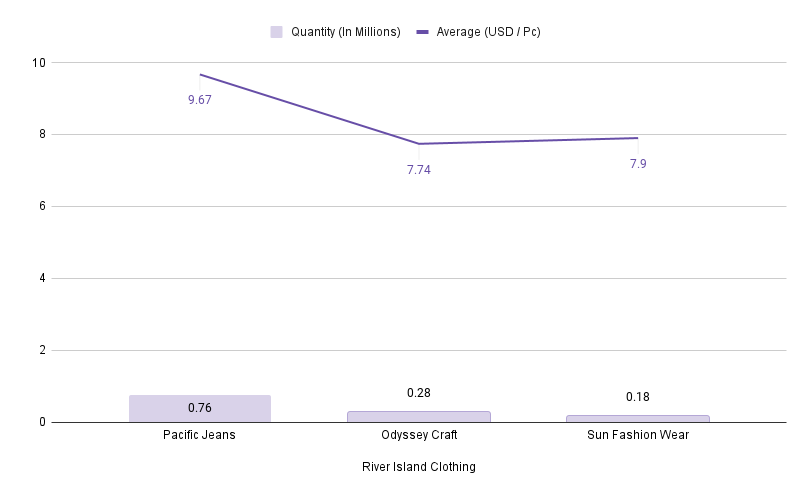

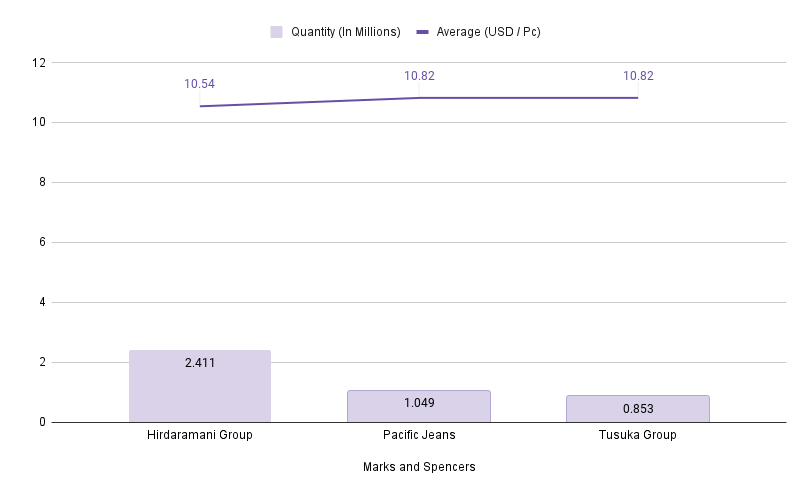

Hirdaramani Group and Pacific Jeans

- Both catered to Marks and Spencer with 2.4 million and 1.049 million units, respectively, at a premium average price exceeding USD 10.50 per unit, reflecting Marks and Spencer’s emphasis on quality. Pacific Jeans shows versatility by also supplying River Island with 0.76 million units at USD 9.67 per unit, suggesting a flexible operation catering to different market tiers.

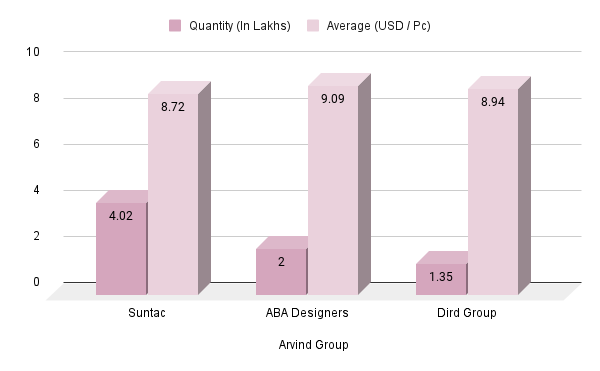

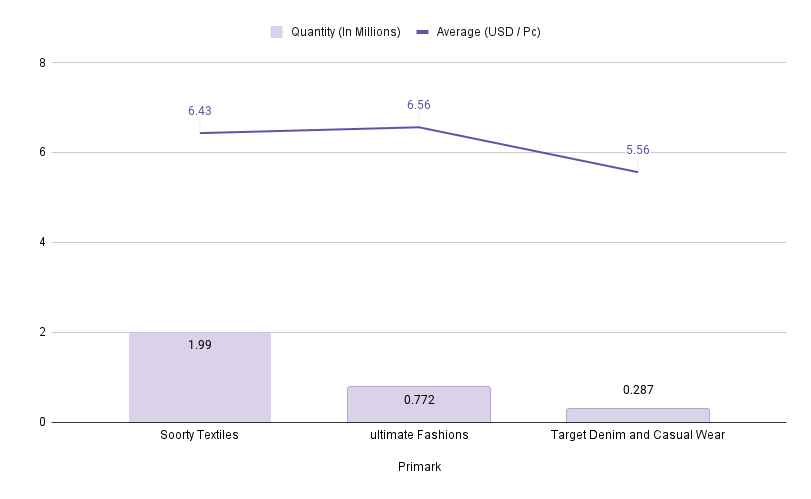

Soorty Textiles

- A major player for Primark, providing 1.99 million units, combining high volume with a relatively low average price of USD 6.43 per unit, aligning with Primark’s affordability strategy.

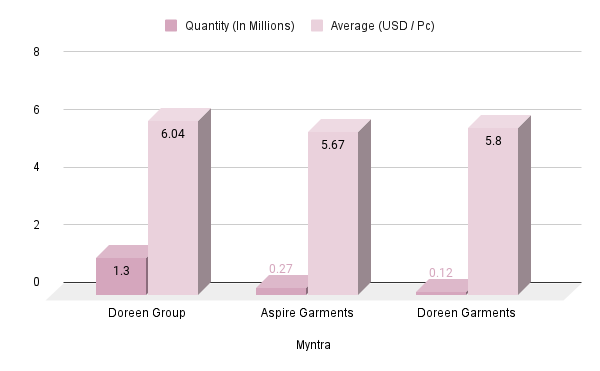

JTC Group and MidAsia Group

- Supplied New Look with 1.37 million and 1.26 million units, respectively, with average prices around USD 7.00 per unit, indicating a mid-market positioning.

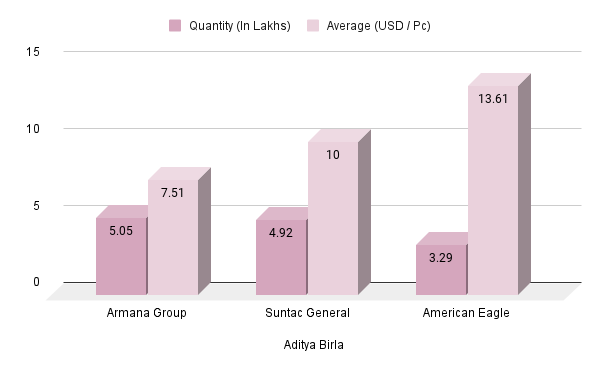

Overview

- Largest Volumes : Next and Marks and Spencer are the largest recipients, indicating their dominant market share in the UK denim sector

- Highest Prices : Marks and Spencer stands out for paying the highest average prices, which likely correlates with their brand positioning towards higher quality merchandise

- Best Value : Primark achieves the best value proposition, balancing large volume procurement with lower average prices

The substantial total of over 33 million units acquired by UK brands, with a dominant 90% attributed to major players, showcases not only the scale of operations but also the strategic alliances with suppliers. Brands such as Next, Marks and Spencer, and Primark have each carved out their niche through volume, value, and a blend of both strategies. [/private_special]

Check out the other reports below: